Business Judgment and Valuing Impacts

Introduction

About twelve years ago, when we first wrote about the relevance of social and environmental information to corporate governance[1], scholars and practitioners alike raised three main issues: Why is social-environmental information a relevant legal and accounting problem?[2] How can “non-financial” issues be measured? Should they be relevant and measured for decision-making? In the meantime, many jurisdictions have adopted legal norms or practice guidance on issues concerning sustainable governance. Despite the recent pushback (Eccles, 2023)[3], ever since the UN Global Compact, the UNEP Finance Initiative, and the Taskforce on Climate-Related Financial Disclosures a new consensus has emerged: Board members and executives are not just permitted to consider social-environmental issues, they are expected to do so in their strategy and leadership work and required for compliance, reporting, and risk management.[4] Similarly, corporate entities cannot avoid liability by simply applying the three lines of defence to reputational and operational risks.

At the same time, impact valuation significantly matured in the last two decades from an economic policy analysis tool to a method of accounting for corporate impacts. In this article, we formulate our key challenge and argument of what measurement and valuation of corporate impacts means for the research and practice of corporate governance. We provide evidence to our argument based on a series of three sprints with companies – a new cross-sector collaboration method for agile sustainable development[5] – that deal with the three questions above: Why, how, and if valuing impact has a bearing on business judgment and wider issues in what we call sustainable governance. In so doing, the sprints initiate three pathways of reengagement, recalibration, and realignment of corporate governance with a systems view of corporate value and impacts.

Key Challenge and Argument

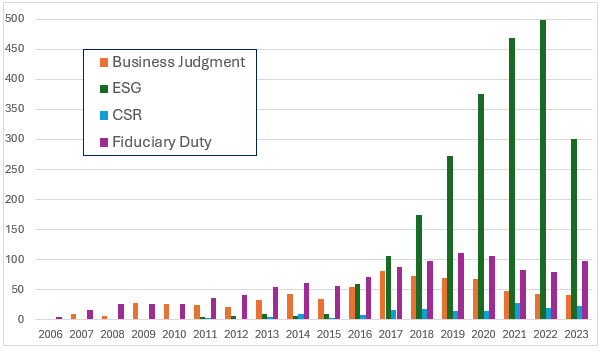

Our analysis of articles on the Harvard Corporate Governance Forum published since 2006 reveals the following long-term trends: themes of legal norms and corporate structures around directors’ duties and business judgment have been outpaced by disclosure of “environmental, social, governance” disclosure, and in turn, gained disproportionate attention over corporate social responsibility in the academic and professional discourse. Upon close reading, a gap widens between academic scholarship on the one hand, and the fields of practice and policy on the other. The former kept a broad view on issues from fiduciary duty and control liability, whereas the latter focused on disclosure and a delineation of “non-financial” against “sustainability-related financial information”.

Figure 1: Number of Articles Published on the Harvard Corporate Governance Forum on Sustainable Governance between 2006 and 2023

Our main argument here is simple: Impact measurement and valuation – making sustainability information useful for rational corporate decision-makers – limits the discretion of board members and directors about how to consider social-environmental impacts. While the inferences, deliberations and conclusions from sustainability information still enjoy broad managerial discretion, impact measurement and valuation – i.e. their methods, processes, and standards – are not covered by business judgment exemptions.

Consider the following three tests for impact valuation as a basis for business judgment:

- Does the rational decision-maker require protection by corporate law to preserve the discretion in considering social-environmental issues for corporate management?

- Does the rational decision-maker use methods and processes for measurement and valuation of social-environmental impacts in their business judgments?

- Are those methods and processes based on generally accepted (international) standards informed by state of the art and science and duly set in the public interest?

If the answer to those three tests above is yes, then the business judgment rule or any equivalent exemption in other jurisdictions does not cover the measurement and evaluation of corporate impacts that form the basis of business judgment. Our broader challenge is that the corporate governance community has not yet entered a stage of theorizing, investigating, and debating the core elements of sustainable development with a view of the entire corporate governance system. What does it mean for the concept of the rational decision-maker? Materiality and price sensitivity? Control liability? Auditor liability and assurance levels? Governance and funding of standard-setting organizations? Conflict of interests and market behaviour?

Of course, there are many more issues. But we argue that in an age of hyper-rationalization of corporate responsibility for social-environmental issues through reporting, measurement, and artificial intelligence, our contribution is to refocus the discussion on business judgment as valuing impacts. Disclosure is not an end in itself; it should just be a means to the end. Upon close reading of the work of the research and practitioner community, we build on the body of knowledge developed in the social science studies of law, accounting, and organizations. The regulators around the world perhaps rely on disclosure because it seems the most politically expedient and least interventionist form of regulation and governance. In the world of practice, a higher awareness of the interconnectedness of impacts, risks, and opportunities, has led to a change of this traditional view. In the world of academia, the problem of the “strength” of the efficient market hypothesis in law and economics finds its correlate in sustainability science on the “strength” of sustainability.[6]

Considering the important contributions in this Forum – Barker and Mayer (2017, 2019), Strine (2019), Bebchuk and Tallarita (2020), Roe (2021), Herren Lee (2022) to name a few[7] – we outline how the next step of the journey could look like. We propose to move on from a pure stakeholder view – which is firm-centric – and climb up to a systems-level view of corporate governance where the dynamics of sustainable development reveal themselves in the flows and stocks of multiple forms of capital: financial, natural, human, and social.[8] Finally, based on previous empirical, theoretical, and normative work, we put forward our definition: Sustainable Governance “involves the set of relationships between a company’s management, its board, its shareholders and other stakeholders”[9] to embed sustainability into the “system by which companies are directed and controlled.”[10] Corporate sustainability is the integration of environmental and social issues into corporate governance systems – frameworks, policies, rules, and procedures for control, risk management, due diligence, and reporting – in both directions: the impact of social and environmental risks on the corporate entity and the impact of corporate activities on society and the environment.[11]

Sprint #1: Reengaging Professional Experts with Judgment on Corporate Value

Our audiences are surprised when we tell them that innovative forms of accounting have already been explored before. We do not need to go as far back as thousands of years to the fabled Code of Hammurabi or hundreds of years to Luca Pacioli who is incorrectly claimed as the ‘father’ of accounting. In the 1970s, so within the lifetime of many distinguished authors in this Forum, a form of Value-Added Accounting has been attempted to reflect the contribution of the workforce to the creation of value in UK companies. The “failure” of this accounting change has been studied in accounting research (Burchell et al 1985).[12] The lesson for today is that corporate sustainability disclosure is subject to the same forces in the social and economic system: the macro-economic environment, industrial relations, and accounting policy.

In our pilot sprint held in early 2023 between teams at the University of Oxford and the Hong Kong University of Science and Technology, we sought to establish a way of collaboration between professional experts. We developed and adapted the sprint method for challenges such as climate change or other social-environmental issues relevant to corporations and their employees (i.e. the professional experts building the relevant knowledge base in organizations and entire sectors). In the context of impact valuation, we sought to define more clearly what standard-setters leave it at the discretion of market participants: decision-usefulness.[13] Impact valuation can provide a clearer distinction between questions of law and fact – the key problem underlying all discussions around the principle of materiality; a principle that is fundamentally about a rational decision-maker’s behaviour of comparing between options: in the role of an investor (buy or sell shares, hold or engage, etc.), a corporate manager (make or buy, cooperate or compete, etc.), or another participant in the economic system such as different stakeholder groups of a firm (object, agree, collaborate or boycott etc.).

Impact valuation forces the research and practice community in corporate governance to think harder about decision-usefulness and business judgment. As a set of indicators for measurement and valuation methods, impact drivers such as Greenhouse Gas Emissions (GHG) or Occupational Health and Safety incidents (OHS) connect sustainable finance and sustainability reporting to corporate governance in several ways:

- Methods: developing measurement systems and tools that are useful to decision-makers

- Processes: designing management systems and processes that manage information flows

- Standards: agreeing on normative expectations for governance and accounting systems

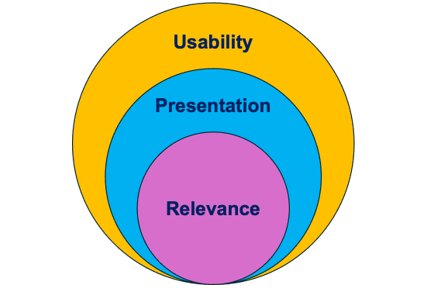

An important outcome of this pilot sprint#1 is a proposal for a new way of thinking about decision-usefulness from a systems and user perspective in what we term information user perspective. Thus, the core elements of user experience for impact measurement and valuation are: relevance, presentation, and usability. Analogously to using sprints in the realm of cross-sector collaboration, we adapt the idea of user experience to corporate information features. First, the interpretation and understanding of the underlying norms of the reporting by the user – e.g. the GHG Protocol for scope 1, 2, and 3 emissions or GRI 403 for health & safety incidents of employees in their own operations and the supply chain – determines the relevance. Second, structural issues – formatting, numbering, naming and unit conventions, the detailed use of abbreviations and words such as “shall”, “may”, “could”, “would”, “should”, etc. – are defined by generally accepted reporting frameworks under (fair) presentation. Thirdly, the context of the decision-maker builds the core of the usability of corporate information. Organizational activities such as capital allocation, product development, sales, investor relations, procurement, etc., they turn information into action and match problems and solutions at different points in time of the organizational decision-making process.

Figure 2: Information User Experience: Qualitative Characteristics aligned with Financial and Sustainability Reporting

Sprint #2: Recalibrating the Decision-Usefulness of Measuring and Valuing Impacts

Since we first wrote about this topic in 2013, the “how” of impact measurement and valuation has evolved to an unprecedented stage of maturity that is almost invisible to the public eye. The technical work also involves policy-relevant choices that shape the information ecosystem. Therefore, the Sprint #2 followed in early 2024. The sprint goal was to provide an overview of impact valuation at sufficient depth and breadth. We ran this cross-sector collaboration initiative –the Valuing Impact Sprint – on a voluntary basis with over 40 participants from multinational businesses, development finance institutions, investors, and professional service providers.[14]

In the ever-evolving landscape of sustainable governance, impact monetization emerged as a method that goes beyond conventional metrics such as profits. Impact valuation approaches can differ depending on the underlying rationale and measurement: costs and (co-) benefits, well-being, damages, abatement, replacement, remediation, opportunity costs, etc. In this diversity of methodologies, the goal sprint#2 sought to engage pioneering impact valuation service providers and corporate experts from different sectors to better understand the connections between their impact valuation frameworks, approaches, and calculations.[15]

Environmental impact valuation covers a wide range of factors, from greenhouse gas emissions to land use and biodiversity. In particular, the providers have some sort of alignment covering GHG, other air emission, but if it gets towards water consumption and pollution, waste, and land use discrepancies emerge. Social impact valuation, on the other hand, assesses parameters such as occupational health and safety (OHS), wages, and diversity, equity, and inclusion (DEI). Here. different assumptions are used and the main difference is between approaches that value OHS, wages, training, and DEI separately and other models that wrap them up under the broader categories of human and social capital.[16]

The output of the Valuing Impact Sprint – a 286-page document with executive summaries and details for specialists – represents an important step towards integrating impact valuation into business, finance, and policy. By exploring and understanding how value factors are constructed and how different methodological choices refer to various decision user cases, the participants have paved the way for more informed decision-making and sustainable investment practices.

In the sprint review, the participants emphasized the need for an information user-centric approach, increased transparency in value factor methodologies, the measurements of fundamental flows and stocks, development of specific user cases in business decision-making with real-world examples and published results. The sprint itself has spawned into further projects and studies that clarify and specify the link between business judgment and impact valuation. Further work that directly or indirectly followed from this sprint has influenced by participants in this Valuing Impact Sprint #2:

- A user case for using impact valuation for Double Materiality Assessment by Deloitte [17]

- A user-friendly Impact Valuation Framework by GIST Impact and WifOR[18]

- A renewed focus on information users in the development of Transparency Criteria for Value Factors by the Global Value Commission[19] and the Governance Framework for Impact Valuation with the Capitals Coalition

It is, therefore, important to further advance our scientific understanding of the behaviour and preferences of information users. Their user profiles may be predictive of how they address uncertainty of the dependencies and impacts across and within industries. Further work needs to be be undertaken in the public interest to ensure the accuracy, comparability, relevance, validity and reliability of impact measurement and valuation. Scaling adoption across industry sectors, jurisdictions, and geographical regions will depend on a favourable constellation between global sustainable development, industrial and stakeholder relations, and (global and local) accounting policy.

Sprint #3: Realigning Asset Owners and Beneficiaries around Value and Impact

Finally, we come back to our analysis of articles that reveals a certain recursiveness of the academic and practitioner discourse since 2006. Note that, up to this point, we have managed to write about sustainable governance without any acronyms of CSR or ESG that mainly follow the trajectory of fashion trends. In practice, CSR as governance issue has always had an existence at the fringe. Yet in academia, it was a long-standing subject related to corporate governance (Waddock and Graves, 1997; Flammer, 2012). Its reincarnation as ESG engaged the traditional corporate governance disciplines of law, finance, and economics on both the academic and practitioner side. Then, ESG experienced the peak of a hype (Serafeim& Yoon, 2022)[20] until it took a path of more critical assessment (Edmans, 2023; Berg et al 2022; Pucker and King, 2022).[21]

Such innovation and learning processes are non-linear and ambiguous. On the one hand, ESG – through the integrated reporting movement – has translated CSR into the language of business and, thus may have fertilized the ground which the idea of sustainable governance could grow on (Eccles and Krzus, 2014).[22] On the other hand, it may have followed a macro-trend from the “audit society” to surveillance which displaced the primate of decision-making and demoted business judgement to a supporting role of quantification and verification (Power, 2022).[23]

Impact valuation takes the corporate governance discourse into a different direction: back to the user of information but also further into the value chains of investors and companies. In June 2024, we have set out to embark on the planning for the next sprint. We conducted several sessions of Valuing Impact Conversations with leading practitioners and researchers. What emerged was a sense of a problem that has been identified since the GRI’s launch by CERES in 1997 and the UNEP Finance Initiative’s landmark report in 2004:[24] The challenge of collective capital – pension, insurance, and mutual funds – to integrate social-environmental impacts systematically in their long-term investments. Investors and regulators have increased their activity in this area in various jurisdictions but with mixed success so far.

We encourage an interdisciplinary field of sustainable governance to address new sets of issues:

- The innovation of legal systems and concepts across multiple forms of capitals: human, social, natural, and financial capital

- The relationship between value creation and sustainability-related regulation and governance of business entities from asset owners, managers, beneficiaries, and creators

- The effect of organizational networks on the information behaviour and decision-making of board members, corporate managers, advisors, and influential investors

- The emergence of information ecosystems: standard-setters, research institutions, service providers, non-profit organizations from business and civil society

- The role of professional communities: lawyers, law firms, corporate counsels and secretaries, accountants, strategy consultants, investment managers, scientific experts

To move from a firm-level to a systems-level view of impact, we propose to pay closer attention to some of the following five interrelated sensitive intervention points in the corporate governance system:

- The interrelations between pension funds, its members, asset managers and advisors, and their multiplier or cascading effect across global value chains.

- The integration of scientific consensus on risks of climate change. biodiversity loss, and social inequality into the investment management of collective capital funds

- The moving landscape of evaluating responsible business – a shift from sustainability scores and ratings to impact valuations and quantified materiality assessments

- The reconciliation of a stakeholder-shareholder view on the firm-level and systems view on corporate governance

- The shift in attention from preparers of sustainability data to the users of information

Therefore, the goal of the next Valuing Impact Sprint#3 is to realign asset owners and beneficiaries. Our sprint will focus on producing concrete prototypes – guidance and user cases – that demonstrate how impact valuation can be integrated in global portfolio management of investments along transition pathways to net zero by 2050. For this next 8-week endeavor at the beginning of 2025, it is important to identify the participants and roles for cross-sector collaboration to achieve this sprint goal. We will improve following the lessons from sprint#2 and will transfer the management of the sprints to an effective and independent non-profit organization. This cross-sector collaboration is committed to work in the public interest and operate under the auspices of a network of leading academic and professional experts.

Figure 3: The Valuing Impact Sprints for Collaboration on Sustainable Governance

among Experts in Science and the Professions

Conclusion

In this article, we propose a way of thinking about business judgment and impact valuation that reconnects the core idea of sustainability to the key concerns of the corporate governance research and practice community. From this common point of departure, we can understand impact measurement and valuation as the next wave of diffusion of social-environmental issues in the system that governs how corporations create, own, and manage capital: sustainable governance. We encourage future empirical, theoretical, and normative inquiry into sustainable governance generally, and impact valuation specifically.

Global standard-setting faces several problems from organizational boundaries to the data quality. As metrics are ambiguous and often ill-defined, thus, questions of law and fact are often conflated and misunderstood, leaders in policy, business, and civil society rightly ask the same question in different ways: how to move from reporting to decision-making? We translate this call from practice into the academic discourse as: How do board members and executives make decisions about impacts, and what information do they need? We encourage this community of research and practice to be inspired by some of the ideas and questions raised here. Impact valuation is not a panacea for all sustainability problems. But it makes the impact drivers mandated by reporting standards such as the International Sustainability Standards Board, the European Sustainability Reporting Standards, or (in future) the US SEC – decision-useful for those behind the steering wheel of corporations: rational decision-makers. In times of increasing requirements for reporting procedures and decreasing resources for sustainability work, effective collaboration – in a constellation between the world of science and the worlds of business and policy – is needed more than ever.

EIN Presswire does not exercise editorial control over third-party content provided, uploaded, published, or distributed by users of EIN Presswire. We are a distributor, not a publisher, of 3rd party content. Such content may contain the views, opinions, statements, offers, and other material of the respective users, suppliers, participants, or authors.